July 30, 2026

Iranian Retaliation Reaches Damietta: A New Front Opens Beyond the Gulf and the Red Sea

Iron Man versus Terminator

What’s inside?

If the machines were to attempt a takeover one day, I’d like to think that technology controlled by humans would still be able to win the day; that our Iron Man suits would be more than a match for the Terminators seeking our destruction.

When it comes to marine insurance, there are similar – though less apocalyptic – concerns about the impact of technology: will artificially-intelligent machines replace humans, or will technology simply make them better?

At Windward, we stand firmly in the second camp: technology will make people better at their jobs. But it will probably also mean historically defined practitioner roles change more quickly.

Excess capacity may provide an additional catalyst. It’s meant that crucial rate increases haven’t materialised and led to a wave of consolidation in the industry. Put simply, it’s still extremely difficult for insurers to make money. So it’s even more important for brokers and insurers to demonstrate added value, perhaps leading to a blurring of the lines between underwriters and brokers as they each adopt a risk advisory role with the client.

Going Deeper

The marine hull market has traditionally evaluated risk on the basis of a series of static features such as vessel type, tonnage, age, flag and ownership. Port state control detentions are also taken into account by some, providing an extra layer of distinction within seemingly ‘similar’ vessels and fleets. A deeper understanding of how a fleet behaves has to date been solely based on the underwriter’s own knowledge of the fleet’s operation: familiarity with the operator, company ethos and track record.

Thanks to technology, that’s no longer the case. The adoption of operational profiles in analysing vessel behaviour is a departure from the traditional way of looking at fleet risk. In many cases the analysis will reinforce the underwriter’s deep understanding of a particular fleet and his intuition on new risks. However, it will also provide a fresh perspective on a fleet’s risk drivers based on its operational history. This facilitates a risk score based on more than just the static features of the vessel and operator. For example, the operational profile might highlight that a particular fleet was spending an above average amount of time in extreme weather, making its vessels 3.5 times more likely to suffer mechanical breakdown.

Similarly, ships spending longer periods in congested traffic lanes are twice as likely to have a collision. Such insights are especially valuable against a backdrop of fewer large claims, but higher overall costs per claim. This way, a granular view of risk can facilitate improved risk selection, distinguishing between fleets which otherwise might seem similar.

The data itself is all in the public domain: things like AIS transmissions, satellite imagery, weather, nautical charting as well as traditional ‘static’ vessel data can all be acquired. The difficult part is making use of it. But it’s worth it.

Big data analysis can provide invaluable insights into the operational profile of a fleet of ships; it can keep the risk advisory role relevant and at the forefront of the industry. Artificial intelligence can augment the risk underwriting process, enabling insurers and brokers to provide their customers with a deeper insight into risk and provide a clear undeniable added value.

It may not be as exciting as an Iron Man suit, but in a soft market, new technology can help marine insurers really show their mettle.

Nick Maddalena is Windward’s Head of Insurance Business

Explore more

Introducing GPS Jamming Resilience: Cutting False Vessel Activity From Contested Waters

Windward is releasing GPS Jamming Resilience, a new platform capability that automatically identifies and suppresses the false vessel activity generated by GPS interference, before any of it reaches an analyst. It launches already proven. Since Operation Epic Fury began in late February, the capability has filtered more than 2.2 million false ship-to-ship (STS) meeting records...

Read More

Ground Truth: Windward’s 2026 Commitment to Verified Maritime Intelligence

By Ariel Zibziner, VP Business Services, Windward Data Integrity in an Era of High-Frequency Signal Manipulation As we conclude 2025, the maritime domain is characterized by a trust deficit in digital signaling. The convergence of major global conflicts — continued hostilities in Ukraine, Houthi attacks disrupting Red Sea transit, suspected infrastructure sabotage in the Baltic,...

Read More

Windward Launches WhatsApp Integration for Instant Risk Insights

At a Glance Redefining Vessel Screening for a Real-Time World In global trade and shipping, decisions are rarely made from behind a desk. A call from port control, a sudden request from a counterpart, or a time-sensitive deal can trigger the need for immediate screening. Whether it’s a compliance check to prevent sanctions breaches or...

Read More

Navigate 2025’s Maritime Risk Landscape with Maritime AI™ at London International Shipping Week

As the global shipping community gathers for London International Shipping Week (LISW) 2025, one reality stands out: disruption is the operating environment, not the exception. The maritime ecosystem is under sustained pressure, and adapting to this high risk era is now a prerequisite for business continuity. From sanctions and signal interference to fraudulent documents and...

Read More

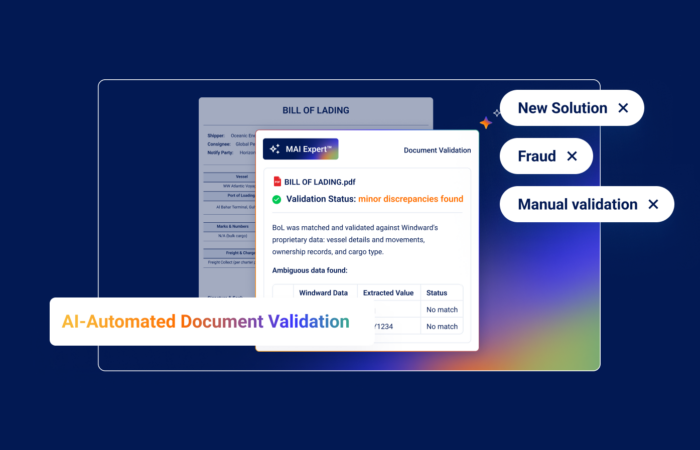

AI-Automated Document Validation: Streamlining Trade Against Real Maritime Activity

Global trade still runs on paper. Bills of Lading, certificates of origin, price attestations, and other documents remain the backbone of maritime trade, yet also its most persistent Achilles’ heel. Forged paperwork fuels fraud, delays compliance, and stalls cargo worth millions. Windward’s new AI-Automated Document Validation changes that, by cross-checking every document against what actually...

Read More