May 25, 2026

Trump Says Hormuz Will Open: A Deal Takes Shape as Iran Expands the PGSA

From Risk Platform to Collaborative Ecosystem: Reducing Friction in Chartering

What’s inside?

By Ami Daniel, Co-Founder & CEO, Windward

When we founded Windward.ai in 2010, we were a small startup of engineers and maritime experts using AI to bring order to chaotic oceans. Today, with nearly 300 customers — including governments, shipowners, energy firms, insurers, and traders — our Maritime AI™ platform influences billions in daily trade. Regulators use it for high-risk vessel profiling, dark fleet tracking, and protecting underwater infrastructure like cables and pipelines.

Our growth reflects a more complex world: geopolitical tensions, shadow fleets, and surging sanctions. Risk scores from our platform now carry real weight, but they demand responsible resolution to avoid delays in time-sensitive markets.

Geopolitical Storm: Data-Driven Insights

Geopolitics is turning the world’s shipping lanes into contested grounds. Wars, territorial disputes, shifting trade policies, and illicit flows (from sanctions-busting crude to fentanyl and human trafficking), are colliding to create mounting uncertainty at sea.

Russia’s invasion of Ukraine, tensions with Iran, and flashpoints across the Asia-Pacific are just a few of the forces that are upending economic and operational stability, as shadow fleets adapt and regulators race to keep up.

Here’s the data:

- Tanker Sales Surge: Before 2022, annual secondhand tanker sales averaged 200-300 vessels. Following Russia’s invasion of Ukraine sales jumped to over 600 in 2022, 495 in 2023, and 268 in 2024 (for vessels over 20,000 dwt). Over the same period, Russia’s shadow fleet expanded from fewer than 100 vessels in early 2022 to 300-600 by early 2025 — a 2-3x increase driven by sanctions evasion.

- Scrapping Rates Plunge: Historically, 25-140 vessels were scrapped each year. Post-2022 scrapping fell to 27 in 2022 (1.5M dwt), 13 in 2023, and just 11 in 2024. Older ships are being retained for illicit trades, increasing opacity.

- Sanctions Explosion: In Q1 2025, newly sanctioned vessels rose 40% compared with Q2 2024, with tankers making up 88% of the total. The U.S. issued over 1,700 Russia-related designations in 2024, while the EU reached its 18th package by July 2025. UK and Australian designations are now several times higher than pre-2022 averages. Diverging enforcement approaches (e.g., OFAC vs. EU/UK) are creating compliance challenges.

- Deception Tactics Boom: Windward flagged over 3,400 GNSS manipulations on nearly 1,000 vessels (80% in the Persian Gulf). GPS jamming is affecting 14,000 ships each quarter in the Red Sea and Persian Gulf. Advanced methods like AIS handshakes, zombie vessels, and identity laundering – compound distortions, making vessel data unreliable without proper context.

These factors complicate ownership, intent, and activity verification. A tanker near Venezuelan waters might trigger false alarms despite valid licenses which only its operator will have. Siloed processes — emails, calls — waste time and repeat efforts. Off-the-shelf SaaS platforms by definition do not have access to customer data needed for accurate risk insights.

Evolving to Collaboration: A New Approach

In the first six months of 2025, hundreds of parties approached us to collaborate and share trade documents. Our supply chain customers – including Scan Global, Rhenus, and others – are already using our products to actively analyze documents, contracts and tariffs with AI.

We’re now shifting from pure risk detection to a collaborative ecosystem, empowering the industry to resolve issues transparently and efficiently. Starting with existing customers:

1. Proactive Fleet Insights: Existing customers will get exclusive access to weekly previews of updated sanctioned, dark, and grey fleet lists — five days before release — for early review and action.

2. Pre-Publishing Collaboration: Share vessel-specific documents (e.g., ownership certificates, compliance waivers) before flagging. You bought an old tanker? Reach out and share it. You know the AIS was off because there was a malfunction? Ping our customer success team. Our experts review, discuss, and adjust to prevent unwarranted issues.

3. Advance High-Risk Clearance: For sensitive trades such as Venezuelan voyages or lifting of crude from Russia, upload documents (e.g. general license, price cap attestation) in advance. We’ll integrate clearances into your risk views, reducing workflow friction.

4. Forward Deployed Engineers (FDE): Our FDE team will design and implement automated customer workflows to send documents whenever a new license is granted or expires, ensuring timely updates and uninterrupted compliance.

Coming soon: In-platform tools for document uploads, metadata tagging, and secure sharing requests — all confidential and user-controlled. Flags will indicate document existence, enabling easy access without exposure.

The Benefits and Path Forward

This approach is rooted in a lesson we’ve learned over the years: the foundation of our business is trust.

Every meaningful advance we’ve made has been built on trusted partnerships with our customers. The kind where sensitive documents, operational data, and strategic decisions are shared with confidence that they are secured with Windward.

That trust is earned, not assumed. It comes from transparency in how we work, the rigor of our data security, and the shared goal of solving real challenges together. Partners, regulators, and counterparties recognize when processes are both compliant and verifiable. And when customers contribute data, the result is richer intelligence, sharper decisions, faster assessments, and proactive edge in navigating risk.

From our startup roots, our mission endures: AI-driven clarity for the seas. In this shadowy era, let’s collaborate for a brighter future. Contact us to explore how this transforms your operations.

Explore more

Ground Truth: Windward’s 2026 Commitment to Verified Maritime Intelligence

By Ariel Zibziner, VP Business Services, Windward Data Integrity in an Era of High-Frequency Signal Manipulation As we conclude 2025, the maritime domain is characterized by a trust deficit in digital signaling. The convergence of major global conflicts — continued hostilities in Ukraine, Houthi attacks disrupting Red Sea transit, suspected infrastructure sabotage in the Baltic,...

Read more

Windward Launches WhatsApp Integration for Instant Risk Insights

At a Glance Redefining Vessel Screening for a Real-Time World In global trade and shipping, decisions are rarely made from behind a desk. A call from port control, a sudden request from a counterpart, or a time-sensitive deal can trigger the need for immediate screening. Whether it’s a compliance check to prevent sanctions breaches or...

Read more

Navigate 2025’s Maritime Risk Landscape with Maritime AI™ at London International Shipping Week

As the global shipping community gathers for London International Shipping Week (LISW) 2025, one reality stands out: disruption is the operating environment, not the exception. The maritime ecosystem is under sustained pressure, and adapting to this high risk era is now a prerequisite for business continuity. From sanctions and signal interference to fraudulent documents and...

Read more

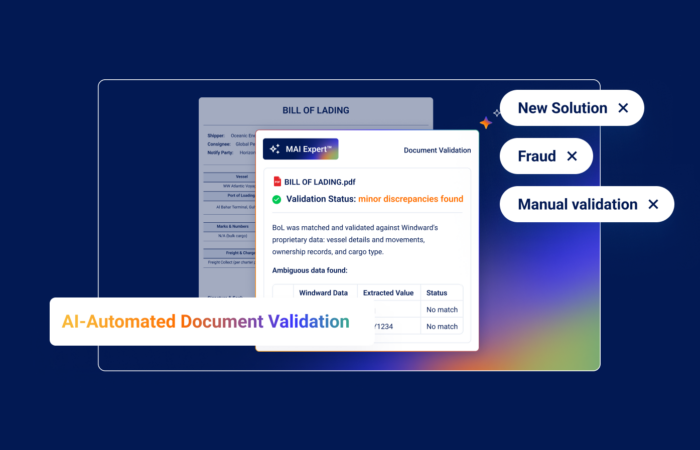

AI-Automated Document Validation: Streamlining Trade Against Real Maritime Activity

Global trade still runs on paper. Bills of Lading, certificates of origin, price attestations, and other documents remain the backbone of maritime trade, yet also its most persistent Achilles’ heel. Forged paperwork fuels fraud, delays compliance, and stalls cargo worth millions. Windward’s new AI-Automated Document Validation changes that, by cross-checking every document against what actually...

Read more