April 29, 2026

April 29, 2026: Iran War Maritime Intelligence Daily

March 8, 2026: Iran War Maritime Intelligence Daily

What’s inside?

At a Glance

- Traffic through the Strait of Hormuz remained near a standstill on March 7, with only three total crossings recorded.

- Selective transit behavior may be emerging, with certain non-Western-linked vessels continuing to move while broader commercial traffic remains frozen.

- GPS and AIS interference intensified sharply, affecting more than 1,650 vessels and concentrating spoofed positions near Fujairah and the Gulf of Oman.

- The threat environment remains active, with reported strikes on the tanker PRIMA and the tug MUSAFFAH 2 reinforcing the continued risk to commercial and support vessels.

- Bab el-Mandeb and Suez traffic remained elevated relative to Hormuz, supporting the view that trade is being redistributed unevenly across regional chokepoints.

- Kharg Island crude export activity remains active, while IRISL-linked cargoes continue moving from China toward Iran.

- Shadow fleet and sanctions-evasion activity continues under the cover of the conflict environment, including the previously identified semi-dark ship-to-ship transfer by M/V TRUST in the Gulf of Oman.

Operational Overview

Traffic through the Strait of Hormuz remained near a standstill on March 7, with only three total crossings recorded and SAR imagery confirming continued lean traffic conditions through the waterway. The small number of successful transits suggests that passage remains possible for a narrow subset of vessels, even as the broader commercial picture remains deeply constrained.

At the same time, the mechanisms suppressing traffic are no longer purely kinetic. The combination of vessel attacks, elevated strike risk, GPS and AIS interference, and the withdrawal of insurable war-risk coverage is now producing a de facto closure effect for much of the commercial market, despite the absence of a formally declared and universally enforced blockade.

A second shift is also becoming visible in the operating environment. Windward analysis suggests that selective transit behavior may be emerging, with certain non-Western-linked vessels continuing to move through Hormuz while broader traffic remains frozen. That pattern is accompanied by continued elevated activity through Bab el-Mandeb, indicating that regional shipping is not normalizing but being redistributed unevenly across chokepoints.

Meanwhile, upstream pressure continues to build. Kharg Island imagery indicates that Iranian crude export operations remain active, while IRISL-linked cargoes continue to move from China toward Iran. Together, these signals indicate that selective transit access, ongoing export activity, strategic resupply, and market dislocation are unfolding in parallel rather than sequentially.

Strait of Hormuz Traffic

Crossings through the Strait of Hormuz remained extremely limited on March 7.

A total of three crossings were recorded, including one inbound and two outbound movements, representing a 25% decrease from the previous day and remaining significantly below the seven-day average of 13.43 crossings.

Observed vessel subclasses included one oil/chemicals tanker, one container vessel, and one bulk carrier. Flag distribution included one Palau-flagged vessel, one Iranian-flagged vessel, and one Liberia-flagged vessel.

Recent SAR imagery captured on March 7 visually confirms the continued scarcity of traffic through the Strait. However, the successful outward transit of two vessels suggests that selective transit allowances may now be in effect.

One of the vessels — a 127-meter Palau-flagged oil/chemicals tanker — has previously been highlighted by Windward as high risk due to multiple identity and location tampering events in Iraqi waters, behavior consistent with Iranian loading typologies. Another vessel – a 190-meter Liberia-flagged bulk carrier owned and managed by Chinese companies — was observed exiting the Strait while broadcasting “Chinese Crew” in its AIS destination field.

These movements may indicate the early emergence of an affiliation-based passage model, under which certain non-Western-linked vessels are able to transit while broader traffic remains effectively suppressed.

Who Continues to Transit Hormuz

Windward analysis of vessels that have continued to transit the Strait during the crisis shows that traffic is dominated by vessels with elevated compliance risk profiles.

Of at least 18 vessels confirmed to have transited since March 2:

- 3 vessels (17%) were sanctioned.

- 5 vessels (28%) were classified as high-risk.

- 2 vessels (11%) were medium-risk.

- 8 vessels (44%) were low-risk.

Overall, 44% of vessels transiting the Strait carried elevated compliance risk, indicating that many operators continuing to transit are not typical risk-averse commercial shipping companies.

Three main cohorts appear to be operating:

- Shadow fleet operators: Sanctioned vessels with limited exposure to Western finance or insurance appear willing to accept the heightened risk environment.

- Iran-linked trade networks: High-risk vessels involved in Iran-related cargo flows appear to be continuing operations under the assumption that IRGC forces will permit passage.

- Regional energy necessity operators: A smaller group of regional vessels linked to Gulf energy infrastructure appears to be continuing limited operations to sustain essential supply chains.

Chinese-operated vessels were also among those successfully transiting, including ships broadcasting AIS messages emphasizing Chinese ownership and crew composition, suggesting attempts to signal non-Western affiliation.

Insurance Withdrawal and De Facto Closure Mechanism

The collapse in commercial traffic through the Strait of Hormuz appears to be driven not only by direct kinetic risk but also by a structural insurance shock within the global maritime risk market.

Following the escalation of hostilities, several major Protection & Indemnity (P&I) insurers issued 72-hour cancellation notices on Gulf war-risk coverage, while reinsurance capacity from London markets was temporarily withdrawn. Without reinsurance backing, P&I clubs are unable to extend coverage for vessels operating in designated war zones.

This mechanism has produced a de facto closure effect across the Strait.

Global maritime trade is heavily dependent on the International Group of P&I Clubs, which insures roughly 90% of the world’s oceangoing tonnage. These clubs rely on reinsurance markets to absorb catastrophic risk exposure. When that capacity contracts or disappears, shipowners may no longer be able to obtain the insurance required to operate in high-risk waters.

Premiums that were previously around 0.25% of vessel value per transit have risen toward 0.5% or higher, and in some cases, coverage is unavailable entirely.

This has had an immediate operational impact. Vessel tracking indicates that dozens of tankers and cargo vessels accumulated in holding patterns near Fujairah and across Gulf waters, while major carriers suspended Hormuz crossings.

The result is that the Strait has effectively shifted from a contested waterway to a market-constrained chokepoint, where the primary limiting factor is no longer solely military threat but also the inability of operators to secure insurable risk coverage.

Bab el-Mandeb and Suez Canal Traffic

Bab el-Mandeb

Traffic through Bab el-Mandeb remained elevated on March 7.

A total of 34 crossings were recorded, including 23 inbound and 11 outbound movements, representing a 47.8% increase from the previous day and sitting significantly above the seven-day average of 9.7 crossings.

The top vessel subclasses included nine bulk carriers, five oil products tankers, and three crude oil tankers. The largest flag groups were the Marshall Islands, Panama, and Liberia.

The continued strength of Bab el-Mandeb traffic, even as Hormuz remains largely frozen, supports the view that shipping is being redistributed unevenly across regional chokepoints rather than normalizing.

Suez Canal

Transit activity through the Suez Canal increased on March 7.

A total of 43 crossings were recorded, including 24 inbound and 19 outbound movements, representing a 59.26% increase from the previous day and remaining above the seven-day average of 36.88 crossings.

Top vessel subclasses included 11 bulk carriers, nine crude oil tankers, and five container vessels. Flag distribution was led by Panama, Liberia, and the Marshall Islands.

Cape of Good Hope Diversion

Transit activity around the Cape of Good Hope remained below normal levels on March 7.

A total of 47 crossings were recorded, including 22 eastbound and 25 westbound movements, representing a 38.96% decrease from the previous day and sitting significantly below the seven-day average of 80.43 crossings.

Top vessel subclasses included 20 bulk carriers, nine container vessels, and four crude oil tankers. Flag distribution was led by Liberia, Panama, and the Marshall Islands.

GPS Jamming Escalation

Electronic interference across the Gulf intensified significantly over the past week.

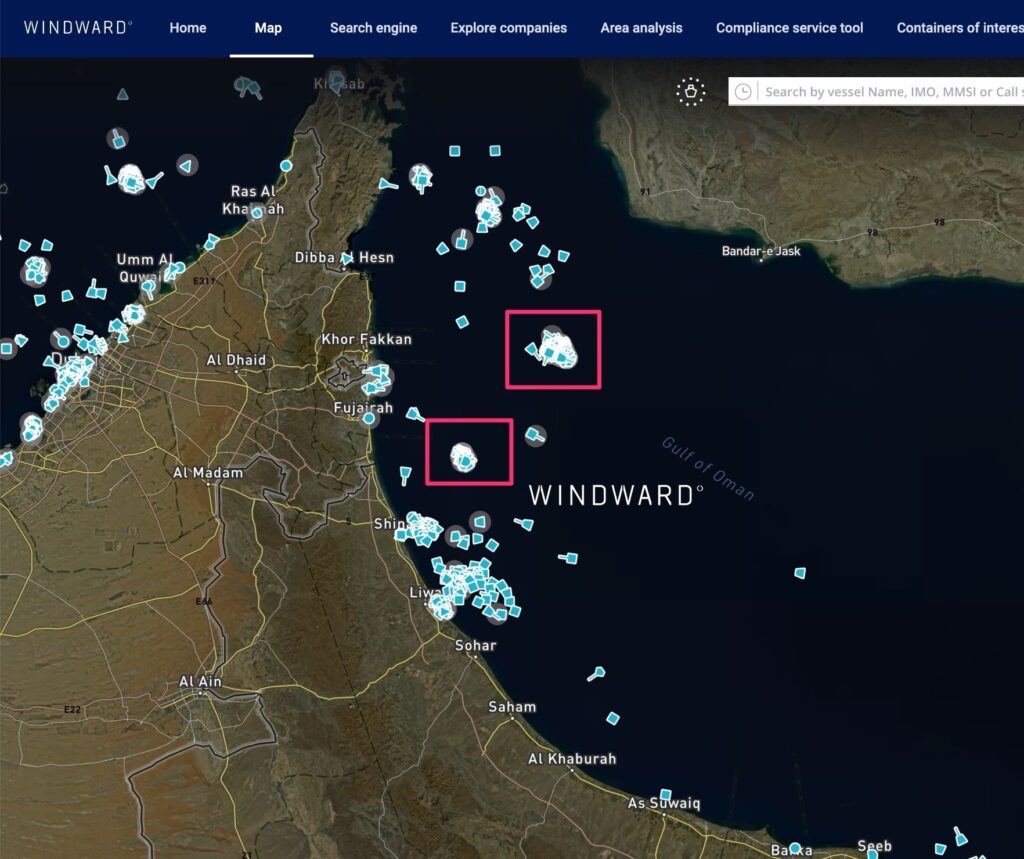

Windward analysis shows that more than 1,650 vessels experienced GPS and AIS interference on March 7, representing a 55% increase compared with the previous week. Vessels were falsely positioned across both land and sea locations stretching from Kuwait through the Arabian Gulf and into the Gulf of Oman near Muscat.

Windward identified at least 30 jamming clusters across Saudi Arabia, Kuwait, the UAE, Qatar, Oman, and Iran, affecting both maritime and onshore signal environments. These clusters have evolved from earlier circular displacement patterns into zig-zag signal distortions, where vessels’ AIS positions are thrown across multiple locations within a 24-hour period.

Persistent interference is increasing operational risk by creating false compliance alerts, degraded navigational awareness, and elevated collision risk in one of the world’s most critical energy corridors.

The interference environment is also contributing to unusual vessel behavior. AIS signals are now clustering hundreds of vessels in concentrated digital locations off the Gulf of Oman, reflecting both signal manipulation and vessels waiting for safer operating conditions.

PRIMA Drone Strike

On March 7, the Maltese-flagged chemicals tanker PRIMA (IMO 9427433), formerly STEPHANIE, was reportedly struck by an Iranian drone while transiting the Strait of Hormuz.

The vessel is a 112-meter chemical tanker owned by Kyotonia Limited of Cyprus and operated by Argo Trading of the UAE since August 2025. Iran’s Islamic Revolutionary Guard Corps reportedly claimed responsibility for the strike, stating that the vessel had ignored repeated warnings not to enter the Strait.

The incident reinforces the continued threat to commercial vessels attempting to transit Hormuz, even as a small number of ships appear to be securing passage without incident.

MUSAFFAH 2 Incident

The tug struck while towing a previously targeted cargo vessel on March 5 has now been identified as MUSAFFAH 2 (IMO 9522051), a UAE-flagged tugboat.

Subsequent reporting indicates that the tug caught fire and sank in the Strait of Hormuz on March 6 following an explosion. The vessel was carrying seven crew members, including Indonesian, Indian, and Filipino nationals. Four crew members survived, while three Indonesian crew members remain missing.

This case is operationally significant because it supports JMIC’s assessment that vessels engaged in assistance, towing, or salvage operations may themselves face elevated risk of follow-on strikes.

Confirmed Vessel Attacks

As of March 7, 11 vessels have been struck since the beginning of Operation Epic Fury:

- Skylight (IMO 9330020).

- Mkd Vyom (IMO 9284386).

- Sea La Donna (IMO 9380532).

- Hercules Star (IMO 9916135).

- Stena Imperative (IMO 9666077).

- Athe Nova (IMO 9188116).

- Ocean Electra (IMO 9402782).

- Safeen Prestige (IMO 9593517).

- Mussafah 2 (IMO 9522051).

- Prima (IMO 9427433).

- Sonagal Namibe (9325049).

The growing list of affected vessels, combined with attacks on anchored, drifting, and assistance vessels, reinforces that the campaign is designed to generate broad operational uncertainty across the maritime environment rather than target only one vessel type or operating profile.

Kharg Island Activity

Recent satellite imagery from March 7 indicates that Kharg Island crude export operations remain highly active despite the ongoing conflict.

Imagery confirms a substantial clustering of tankers both at berth and in the waiting area:

- At berth: 2 VLCCs, 1 Aframax tanker.

- At anchor nearby: 2 VLCCs, 1 Aframax tanker, and several MR tankers.

This pattern suggests that Iranian export infrastructure remains operational and that crude throughput is continuing, even as maritime risk in surrounding waters remains elevated. The concentration of tonnage also indicates a sustained backlog of export activity rather than a terminal shutdown.

Fujairah Bunkering Disruption

The regional bunkering hub of Fujairah has seen a dramatic reduction in vessel activity following attacks on fuel storage infrastructure earlier in the week.

Bunker suppliers have declared force majeure or suspended deliveries, and vessel tracking shows a near-absence of ships at anchor near Fujairah and Khor Fakkan, normally one of the world’s most congested bunkering zones after Singapore.

The disappearance of anchorage traffic is likely the result of a combination of security concerns, GPS interference, and elevated strike risk in congested maritime areas.

VLCC Freight Market

Middle East disruption continues to drive extreme tanker freight pricing.

A VLCC was reportedly fixed on March 7 at a record $770,000 per day, reflecting the market premium now attached to voyages linked to disrupted Gulf export flows. The fixture highlights the growing divergence between physical trade constraints and owner returns for the small number of operators still willing to engage in high-risk Gulf-linked trades.

Russian Price Cap Pressure

The surge in global energy prices is now pushing Russian crude and refined product trades beyond the limits of the Western oil price cap regime.

Wholesale diesel and gasoil prices in Europe surged 54% week-on-week, reaching more than $1,158 per tonne on March 6 — roughly $155 per barrel equivalent — exceeding the $100 per barrel price cap for Russian refined products.

The price spike means that new Russian cargo sales are increasingly non-compliant with the cap, creating potential enforcement challenges for Western regulators and operational dilemmas for tanker operators.

Greek-owned tankers, which historically carried a large portion of Russian energy exports, may face growing pressure to exit the trade if elevated prices continue to push cargo values above cap thresholds.

CAFFA Seizure

The general cargo vessel CAFFA (IMO 9143611) was seized by Swedish authorities on March 6 while sailing from Casablanca to St. Petersburg.

Authorities determined that the vessel’s claimed Guinea registry was fraudulent, effectively rendering it stateless under maritime law. The seizure was linked to a combination of serious safety deficiencies, false-flag documentation, opaque ownership structures, repeated AIS blackouts, and broader links to sanctions-evasion activity.

Windward identified the vessel as part of Russia’s shadow fleet, with a history of repeated name and flag changes, extended dark activity periods, and repeated operations linked to Russian ports.

The vessel had also been linked to the transport of approximately 3,000 tons of stolen Ukrainian grain from occupied Sevastopol to Tartous in July 2025, following an identity change from VETLUGA to CAFFA and a prolonged AIS blackout approaching Syrian waters.

This seizure reflects a broader European enforcement trend targeting vessels engaged in deceptive shipping practices and Russian sanctions circumvention.

IRISL China–Iran Chemical Shipments

Two cargo vessels owned by Iran’s sanctioned state shipping line IRISL have departed the Chinese chemical port of Gaolan and are currently en route to Iran.

Reporting indicates the vessels may be carrying sodium perchlorate, a key precursor used in solid rocket fuel. The ships Shabdis and Barzin departed after loading in Zhuhai and are expected to reach Iranian ports, including Bandar Abbas and Chabahar.

This movement is strategically significant because it suggests that missile-related supply flows to Iran may still be proceeding during active conflict, even as maritime and military pressure on Iranian infrastructure intensifies.

Outlook

The March 8 operating picture shows a maritime environment where selective passage, insurance withdrawal, electronic manipulation, continued strikes, and active upstream supply flows are all shaping the market at once.

Hormuz traffic remains near minimum levels, but recent transits suggest that passage may still be possible for a narrow subset of vessels with lower exposure to Western finance or political alignment. At the same time, GPS and AIS interference has intensified, attacks continue to affect commercial and support vessels, and insurance constraints are preventing much of the commercial fleet from re-entering the corridor.

Meanwhile, Kharg Island export activity remains active, IRISL-linked cargo movements from China are continuing, and alternative chokepoints, including Bab el-Mandeb and Suez, are absorbing unevenly redistributed trade.

Taken together, these signals suggest that the region is not moving toward normalization. Instead, it is shifting into a more selective, more fragmented, and potentially more persistent operating environment.

Explore more

April 29, 2026: Iran War Maritime Intelligence Daily

At a Glance Operational Overview Maritime activity across the Strait of Hormuz remains stable in volume but increasingly uneven in behavior, with full AIS visibility during transit contrasted by a sharp rise in deceptive activity across the broader Gulf. On April 28, transit volumes held steady, with all crossings conducted while transmitting AIS. At the...

Read more

April 28, 2026: Iran War Maritime Intelligence Daily

At a Glance Operational Overview Maritime activity across the Strait of Hormuz and surrounding corridors remains constrained but operational, with moderate transit levels and continued reductions in both vessel count and dark activity. On April 27, transit volumes held at a moderate level following prior fluctuations, while Gulf-wide vessel presence declined, indicating a partial contraction...

Read more

April 27, 2026: Iran War Maritime Intelligence Daily

At a Glance Operational Overview Maritime activity across the Strait of Hormuz and surrounding corridors remains active but uneven, with transit volumes fluctuating under continued enforcement pressure and operational uncertainty. Following the April 25 rebound, transit activity slowed again on April 26, despite maintaining full AIS visibility across all crossings. At the same time, Gulf-wide...

Read more

April 26, 2026: Iran War Maritime Intelligence Daily

At a Glance Operational Overview Maritime activity across the Strait of Hormuz and adjacent corridors is showing early signs of recovery, but under sustained enforcement pressure and continued sanctions-driven disruption. Transit volumes rebounded on April 25 following several days of suppressed movement, with all crossings conducted under full AIS visibility. At the same time, U.S....

Read more

Two Weeks Into the Ceasefire: A Maritime Intelligence Breakdown

At a Glance The Second Week of the Ceasefire at Sea Two weeks after the ceasefire announcement, the maritime system has moved further away from normalization. The first week of the ceasefire established that Hormuz had not reopened to normal commercial traffic. Movement continued, but under overlapping Iranian control and U.S. enforcement. During the second...

Read more